Automating companies is no longer an idea of science fiction. It is a reality in many sectors that affects thousands of people, either because part of their work is related to controlling that software or because they have become unemployed as result of that automation. Most companies that have opted for automation have two objectives: on the one hand, time savings, robots are faster; and and on the other staff cost savings.

Many banks and finance departments of large companies have incorporated the use of software for programming tasks into their work processes. Actions related to accounting of invoices or financial transactions or operations related to data that do not require the intervention of a professional. This process is technically called Robotic Process Automation (RPA).

Process automation in banks is part of a larger scale process known as Enterprise Resource Planning (ERP), closely related to the use of SaaS (Software as a Service) platforms and cloud computing for financial accounting, but also other departments such as production or distribution. In this scenario, banks can reduce costs between 20% and 50%, workflows are facilitated in IT departments, better risk control with reduced human error in operations and a more efficient collection and data analysis for decision making.

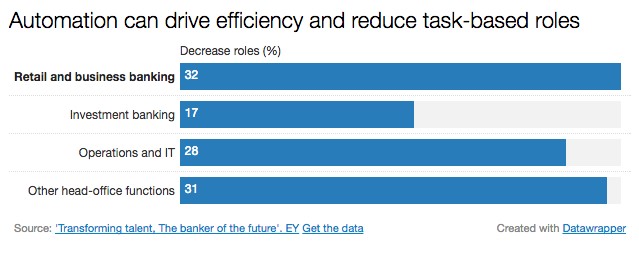

This automation process will cause a substantial reduction in the involvement of people within the operational processes in companies. And banks and financial services are one of the markets most affected, according to figures provided by the report conducted by the consultant EY entitled ‘Global banking outlook 2016. Transforming talent. The banker of the future’:

Fields of banking automation

Today international banking has introduced process-based programming robots in many areas of its business: managing large volumes of data (structured information); common operations with financial products as simple as an account or as complex as a mortgage in greatly reduced times; fraud control; important elements for technology teams as the scalability of resources by demand; and for human resources staff retention.

– Managing large volumes of data: managing Big Data, especially if human error can mean very harmful changes to the banking business, is often placed in different types of software. There is increased precision and decreased risk of mismanagement or a miscalculation: not only in the results of operations, also in erroneous personal data (e.g. names of account holders or their age).

It is customary to leave to software the exchange of data and information between platforms or systems, such as applications or carry out purging of incomplete or wrong data. Also the extraction of the information contained in forms and incorporating it to the actual bank’s systems or updating entries (either income or accruals) in customer accounts. All types of banking tasks are already automated.

Here process automation using robots replaces the work of professionals to grow in efficiency and speed without incurring greater exposure to error, but quite the opposite. It is in such tasks where the software can entail major cost savings.

– Operations with financial products: much of the tasks related to bank accounts, loans or credit, debit and credit cards or mortgages is already automated by software. A common task is what is known as bank reconciliation, a control process by which the accounting records of the entity are matched and those of each personal customer account. This process is usually programmed to save costs, increase speed and reduce the possibility of error.

Requests for credit cards are also often subjected to automation: the customer fills out a web form, the information is sent to the bank’s central unit to be issued. Mortgage approval processes also rely more on software parameters that the criterion of a professional. A third important aspect is the automated warning of loans or personal loans that are in arrears as the customer has not paid. It would be complicated and especially expensive if this task did not depend on a robot.

– Fraud Control: odd transactions often occur in a bank account of a customer that causes an alert in the bank’s employees. That usually initiates an investigation to establish whether the account is being violated and the customer is contacted to determine whether the transactions are really theirs or not. Sometimes charges in other countries are due to fraud. Early warning of this odd behavior is automated with software. Using machine learning techniques to prevent bank fraud is common.

– Increasing the scalability of IT services: all companies in the world, and the banks make up these, very often have peak workloads, either at the end of the month, during the quarterly or annual closing. For banks it is cheaper and faster to grow in software resources (that they can scale and then return to the starting point) than respond to growth in demand with recruitment.

– Retaining talent: one of the main reasons for absenteeism and final abandonment of companies is mechanical, uncreative and unedifying work. Banks resort to software and robots to unload teams of work that would only bring more stress to their professionals. Tasks that in most cases are perfectly programmable using technology.

Technical implications for robotics

Robotic Process Automation (RPA) requires cultural changes in any organization, but also changes in the resources provided by IT teams (infrastructure and security), especially in Business Process Management. BPM is the corporate discipline that automates, executes, measures and optimizes the flow of business activity in support of the objectives of the actual company. And it affects all of the company’s resources: employees, systems, platforms, customers, partners…

It is business process management professionals who must be responsible for adapting new technologies, normally associated with disruptive processes, to the company’s interests: either software or robotics, the Internet of Things or the new era of mobile services and products. The bank of the future will not resemble anything like what we are able to dream about today.

If you want to find out more about BBVA’s financial APIs, go to this website.

If you want to try BBVA’s APIs, test them here.