APIs are the future of automated banking services. Albert Pla, Head of SME eSales in BBVA Global Markets, tells us about this technology.

APIs are one of the newest and most highly anticipated tools in Open Banking. They can automate business processes and allow bank transactions to be carried out without leaving the company’s work environments. They feature applications that make life easier for the corporate customer, embedding the financial services they need in their own work environment, streamlining transactions and decision-making. This process automation also reduces costs.

But what are the advantages of APIs over other systems? What do they involve? How has the market changed, and what is needed to democratize it? With the help of Albert Pla Arasa, Head of SME eSales at BBVA’s Global Markets, we will try to answer these and other questions about the API ecosystem.

Four advantages of using an API in your company

APIs: a way of automating banking communication

In the words of Albert Pla, APIs are the “core product of Open Banking“. They are the second phase of digitization that began with ‘Do It Yourself’ and that has been shaping banking systems with respect to the user, who is increasingly empowered.

This empowerment is now based on automation. APIs allow all types of businesses, including SMEs, to automate their bank processes and spend more time getting work done. This frees up the company’s staff and increases performance for businesses that opt for this technology.

The difference between pre-API environments and integrated systems is that it allows “certain processes to be automated” with other players while ensuring they are accessible by firstly agreeing on common terms that help them to speak the same language.

In other words, the way of communicating has been simplified to streamline procedures, and protocols have also been designed that execute orders sent by the user. This saves employees from performing repetitive and tedious tasks.

“An API is a protocol for exchanging information through a very efficient technology,” explains Pla, through which two contacts “agree on how they will share information, and in which format, fields and language.” It is like choosing a common language instead of translating every phase using a dictionary each time either of the contacts says something. It is immensely useful.

Why use APIs and not another infrastructure?

Technology is there to make people’s lives easier or, as Albert Pla emphasizes, “what we seek is to optimize the time taken to complete a task both personally and professionally”, and APIs allow us “to automate part of the tasks considered less valuable” and spend more time on “value-added tasks”.

In a sense, APIs focus on the logical, calculating, cold and mathematical part of operations, on repetitive and tedious processes. Meanwhile, people can focus on the creative part, on collaboration, persuasion, adaptability, new ideas or management, and allocate resources better.

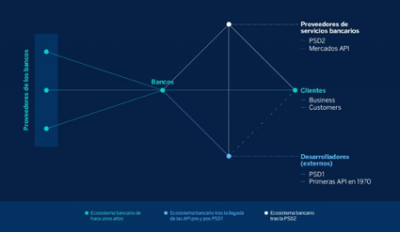

As Albert Pla points out, the competitive edge or main advantage of APIs is that “automation leads to efficiency and, therefore, to cost savings”. This was made possible when PSD2 allowed players such as banking service providers and developers to be integrated within the banking ecosystem (formerly customer-bank), encouraging information exchanges. That greatly simplified API automation.

APIs represent a change in the way customers interact

A few decades ago, banking services were almost only vertical through very limited products and services in an almost linear customer-bank relationship. But with the arrival of Open Banking and the subsequent boost given by PSD2, new alternatives have been born, for example, AIS account aggregation services. The ecosystem has been enriched and the possibilities for the customer have increased exponentially with services previously unthinkable because they were, simply, impossible a few years ago.

With this greater complexity and density of players there has been an increase in specialization which, curiously, has increased the security of the services offered. As Albert Pla points out, now “you know that there is a specialized team that spends all day thinking and working so that all those services that exist, or not, are ready for the market”.

Not only does it mean new tools for end users, but knowing that there is a team of developers in charge of making everything go smoothly with the API in question provides peace of mind, like what happened with the ecosystem of mobile apps when it was built on the network. Specialization is key to a rich and thriving ecosystem. Being the first on the scene is too.

Deploying the API ecosystem

Where there is a market, there is competition, although some players move faster than others. Some Spanish and European banks, including BBVA, have long since created teams specialized in Open Banking, and in recent years new competitors have arrived on the scene.

Albert Pla stresses how “we were one of the first” in Spain in the field of API and Open Banking, so “we are very well positioned”. Having said that, there are already some fintechs, as well as other banks that are starting to develop APIs beyond regulatory ones.

This increase in competition can be good news for all players, as it helps to develop the sector as a whole. The more companies that help deploy the API ecosystem, the richer and more fruitful it will be, and the more useful it will be for the end customer.

Where is the API ecosystem going? What will it be like in the future?

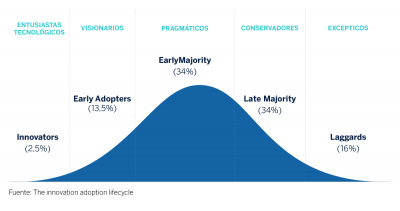

Every technology follows a process called ‘Technology Lifecycle’, which occurs in an ‘S’ adoption curve. While in the early phases, almost exploration and discovery phases, early adopters begin to use emerging and new technology in small projects, during the growth and maturity phase the market knows the possibilities and the tools become common use.

This technology is coming out of that first “initial phase in which it is basically known by few people”, so the next step will be to “mature the API expansion cycle” so that they bring even more value to users who currently do not consider them an accessible tool. For instance, “financial added value” can be provided for companies when the buying and selling of currency is automated, but each company will require tools adapted to its processes.

This is exactly what the FX (Forex) API allows: adapting to companies to automate their currency exchanges. But why does technology take a while to take off? There is not much investment in developing or integrating APIs due to “ignorance” and the questions they raise for potential users. Technology is in a phase where if you are the one proposing these solutions within a company you have to “justify your costs and investments a lot”, especially “the smaller the company is”.

What would help to democratize the implementation of APIs?

Like all technology, APIs have entry barriers, although in recent years these have relaxed due to their usefulness for the end customer, who has been able to see how they can help their business.

These barriers will continue to recede as APIs become easier to use. The big challenge is “how can we make a high quality product, but ensure that a very high percentage of our customers can use it?” In other words, how technology is democratized.

In this sense, education plays a key role. Often these API tools are not used due to ignorance or being considered expensive and complicated, when they have not been for a long time. In fact, accessing APIs now gives companies a considerable competitive advantage, precisely because they are not yet widespread.