Today some experts indicate that conversational bots will be future applications, with an even higher degree of intimacy in their relationship with users. Banking is one of the sectors that is gradually exploring how chatbots can help to improve the financial experience with their customers and how that relationship may lead them to provide better service and gain a competitive advantage over their rivals. There are some notable cases.

Three pieces of data corroborate this:

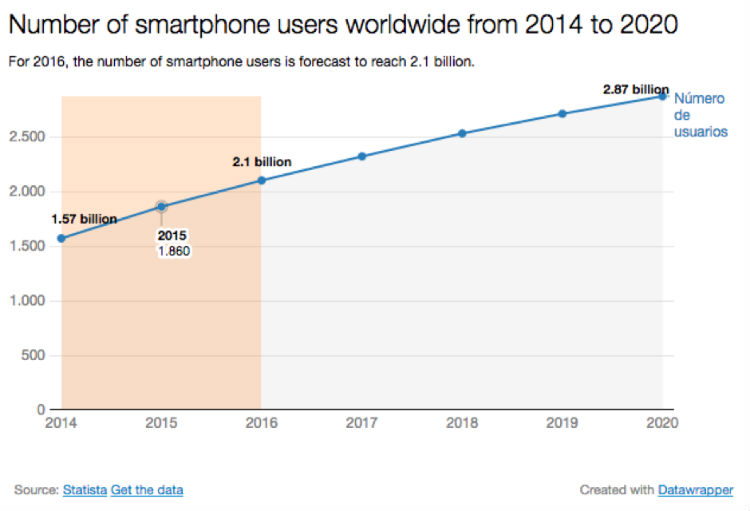

1) The penetration of smartphones in the world market is unstoppable: there are still countries where these devices are being incorporated at a slower rate, but in the rest it is happening at an accelerated pace. By the end of 2016 the number of smartphone users is expected to be 2.1 billion. This graph shows its progress:

2) The growth of instant messaging applications has been extensive: today usage and growth curves of instant messaging applications and social networking applications have already crossed. People are beginning to stop spending their time in social networks and are beginning to move into other products such as WhatsApp, Telegram, Facebook Messenger, WeChat and Snapchat. There is a clear opportunity. WhatsApp has more than 1 billion active users per month. WeChat has somewhat less. Here are a couple of charts by Statista: for WhatsApp and for WeChat.

3) The volume of messages in these applications is growing: if you look at the figures of the increase in the number of active users per month and the total volume of messages in such applications, the future could be promising.

In the end there are two rules that are quite common in the technology market: it is necessary to grow horizontally and reach a certain volume to make money, and it’s impossible to do so if you’re not in the same place as the users. Instant messaging applications, which some big social networks are behind, have launched free tools from which they expect to make money.

What can bots do for banking

There are several types of transactions that no longer need to be carried out by a user through an app and even less so by having to go to the branch. In fact, employees don’t even have to be involved. A bot can perform the following for a bank without the experience losing value:

● Alerts and notifications: banks may use bots to send alerts and notifications to their users on all kinds of operations. They can notify the fact that a payment has been received or their payroll has been paid in to an account, payment of a product or service through the card, payment of any of the bills, etc. Even in minor matters, but important for the experience as support: users who need to cancel, check their balance or request a new PIN fo their debit or credit card, etc. A 24/7/365 assistant bot.

● Customizing the offer: bots are very useful for interacting with users and finding out about them, without being overly invasive, especially if gamification mechanisms are used to achieve this. It is a prerequisite to customizing offers tailored to the customer’s tastes, values and personality, who we often know little about.

● Paying in checks: today there are large companies like IBM with Watson and Microsoft with Azure that have services that enable image recognition applied to financial transactions. It’s as simple as taking a picture of the check where you see the amount of the deposit.

● Person-to-person mobile payments: bots have also become an opportunity for quick payments between friends, without many complications and without any financial institution being involved. There are already some promising cases of such proposals: one example is Mypoolin ChatBot, a UPI (Unified Payments interface) or instant payment system developed by the National Payments Corporation of India. Each UPI is developed on the basis of an IMPS (Immediate Payment Service) infrastructure for transferring money between bank accounts using unique identifiers such as a mobile phone number or VPA (Virtual Payment Address), without the need to use an account number, which creates uncertainty in users.

Chatbots applied to banking

There are some other interesting examples of banking bots that are evidence of what these prototypes can provide banking as a productive sector. MyKai is a chatbot developed by the startup Kasisto, which is known throughout the world for its conversational artificial intelligence platform KAI. In the end, KAI is a virtual smart assistant that interacts with users through mobile devices, instant messaging applications and wearables. Integration with third-party platforms occurs through its API and SDKs. All its advantages are based on a natural language processing engine.

One of the applications that is most strongly committed to the integration of customer-related processes through convesational chatbots is WeChat, especially the market that best knows this instant messaging tool: China. Companies like Facebook, WhatsApp or Telegram are especially focusing on how WeChat succeeded in the Asian market, largely on the creation of small bots that provide services to users such as buying food at home, ordering a taxi, transferring money between bank accounts, etc.

In the end, banks get several interesting advantages with the arrival of chatbots:

● Reduced costs and increased revenue: as user experience improves and processes with which they are linked are faciliated, friction is reduced and operations increase. Charges linked to this whole operation increase income and costs associated with it are reduced to a minimum.

● Increased efficiency: customers can access the answers they need directly, without delays. It saves a lot of time.

Are you interested in financial APIs? Discover all the APIs we can offer you at BBVA